Net Lease Banks: An Evolving Property Type in Today’s Shifting Landscape

The world of commercial real estate has long regarded net lease bank properties as stable and reliable investments. However, as we stand on the cusp of 2024, the traditional dependability of these properties is being challenged. The culprit? A sweeping and industry-wide decline in bank deposits mixed with a regional banking crisis have left a distinct mark on the landscape of these single-tenant properties.

Deposits: The Economic Bedrock

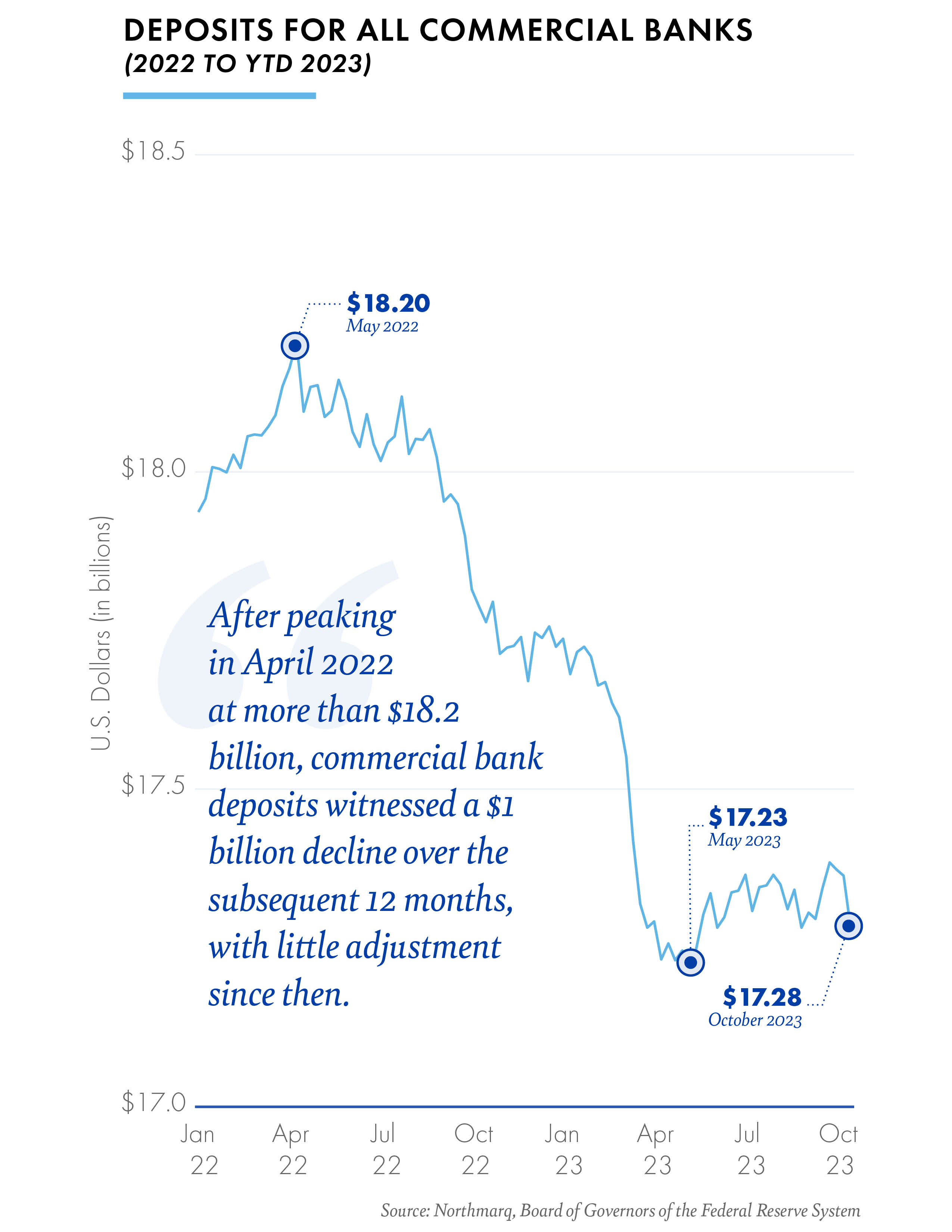

For decades, net lease bank properties were celebrated for their stability. National banks, with their deep pockets, strong credit profiles, and extensive networks, stood as the gold standard of tenants, exuding unwavering financial strength. However, the consequences from the failures of Silicon Valley Bank and First Republic Bank are being felt industry-wide, as consumers recalibrate their trust in financial intuitions. Investors in retail bank properties look at branch deposit levels to gauge the health and necessity of a particular banking location, and those deposit levels have taken a hit in 2023 across the board.

Deposits form the bedrock of a bank’s economic operation. Lending and investment activities, the lifeblood of these financial institutions, are intricately linked to the deposits they hold. If a bank’s branch consistently fails to attract and retain deposits, it becomes less attractive, and the equation of lease renewal takes on a new dimension. We are seeing this dynamic play out in real time – as the largest players in the industry, including Bank of America, Wells Fargo, and JPMorgan Chase, have all recently announced their intention to close dozens of branches amidst volatility in the industry. Property owners with retail banking assets that are either: A) low deposit level branches, B) subpar real estate, C) short lease term remaining, or D) high rental rate locations, need to take a hard look at their investments.

Industry-wide Challenges & the Balance of Bank Profitability

The year 2023 is bringing forth an array of challenges for the banking industry, and a recent report from the Federal Deposit Insurance Corporation (FDIC) underscores the shifting dynamics. It reveals that U.S. banks encountered a staggering loss of $472 billion in deposits during the first quarter, marking the most significant deposit decline since the FDIC began collecting quarterly industry data in 1984. This decline, the fourth consecutive quarter of industry outflows, had a cascading effect across the sector.

Furthermore, the FDIC’s report underlines the impact on a core measure of profitability during the first quarter. As interest rates surged and depositors sought alternative destinations for their funds, many banks found themselves compelled to raise the cost of retaining depositors. This, in turn, eroded the industry’s net interest margins, which represent the gap between what banks earn on their loans and what they pay for their deposits. Put simply, bank deposits are becoming more expensive for banking institutions as they battle higher interest rates. In turn, the banking industry is facing a pullback in profitability that is directly impacting their decision making when it comes time to evaluate extending the lease or shutting down a branch at a particular location.

Navigating the Future in a Shifting Landscape

Evaluating the strength of deposits at a particular bank branch can be difficult, especially with the rise in online banking and how those deposits are allocated across physical bank properties. That being said, banks still use deposit counts, among other important factors, to determine the performance and need for individual banking branches.

A savvy property owner must look not only at deposit counts to evaluate their tenant’s performance but must also take into account industry-wide trends along with sub-market analysis. Outside of deposit counts, banks look to maintain and operate from quality real estate with excellent visibility in markets that are growing. An owner must continuously evaluate the big picture around their real estate investment to ensure that they are taking the right action today to set themselves up to succeed in a market that is undergoing real time change.

Insights

Research to help you make knowledgeable investment decisions