Class B and Class C properties outperforming in the Orange County multifamily market

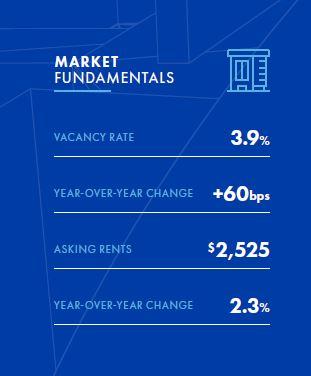

After performing quite well throughout much of 2023, local multifamily properties posted some operational softening at the beginning of this year. Vacancies inched higher, and rents only held steady after three straight quarters of gains. While there was some modest fluctuation at the start of 2024, the Orange County multifamily market continued to record performance that closely tracked the region’s long-term trends. Vacancy closed the first quarter at 3.9%, only slightly higher than the market’s average rate since 2015. With conditions tight, operators are able to either sustain rents or implement modest increases. Construction of new units is accelerating at a modest pace, but Orange County does not face the supply-side pressures that have become increasingly common in many other markets.

Investment activity in Orange County was slow but steady in the first quarter. The number of properties that sold at the start of the year closely tracked average transaction counts that were posted throughout much of 2023, although recent activity continues to lag peak levels achieved in 2021. In the sales that are occurring, transaction prices are largely holding steady. To this point in 2024, the median sale price in Orange County is $390,600 per unit, up slightly from 2023 levels and consistent with pricing trends posted in the region for the past few years. Cap rates trended higher in 2023 but appeared to stabilize in the first few months of this year, averaging between 4.5% and 5%.

Looking ahead

Multifamily properties in Orange County will likely record steady performance in 2024. Renter demand in the area is typically consistent from year to year, keeping vacancy levels tight and allowing for rent increases that generally keep pace with inflation. This year, deliveries are expected to be higher than the recent trend; about 3,600 units will come online, similar to annual averages from 2015-2018. This is expected to result in a modest uptick in vacancy, although much of the forecasted rise already occurred during the first quarter. Still, in most submarkets throughout Orange County, vacancies are unlikely to fluctuate outside of their typical ranges, and rents should creep higher. New deliveries will be concentrated in Irvine and Anaheim, two of the largest employment centers in the region.

Investor sentiment in Orange County is expected to remain positive in 2024, although a few more quarters of limited transaction activity are likely. While cap rates have stabilized, it appears unlikely that they will trend lower to any significant degree, particularly with interest rates stuck in a higher-for-longer holding pattern. Properties that are listed for sale should continue to attract investor attention and trade for elevated per-unit prices. One trend that has yet to emerge thus far in 2024 is the sale of newer properties. Since 2022, sales of newer Class A assets have accounted for approximately 30% of total transactions, but recent sales have been concentrated in rental communities constructed in the 1970s and 1980s.

Learn more

Read the report or contact our Irvine office to learn more.

Read More

Insights

Research to help you make knowledgeable investment decisions