Vacancies inch lower, but deliveries poised to gain momentum in Inland Empire multifamily market

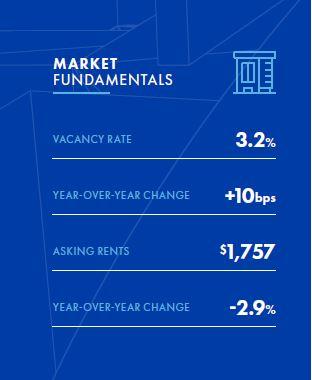

Multifamily fundamentals in the Inland Empire have posted mostly steady results during the past several quarters, and property performance metrics in the first quarter were consistent with long-term trends. The market generally operates at or near equilibrium, with supply and demand closely correlated. During the first quarter, vacancies tightened slightly, following two consecutive quarterly increases in the second half of last year. Current vacancy levels are only minimally higher than one year ago. Rents, on the other hand, have trended lower in recent quarters, including a 0.9% decline at the start of this year. Rents surged in 2021 and 2022 and are now at levels only slightly higher than the year-end 2021 figure. Rents appear to be in a period of modest self-correction but should trend higher in the coming quarters, buoyed by accelerating demand.

Total apartment sales in the Inland Empire at the start of this year closely tracked levels recorded during the second half of 2023. Activity levels are slow, but consistent, reflecting the overall health of property fundamentals, but also the more challenging financing environment. The market appears to have settled into a steady flow of deals; transaction counts in the first quarter were down about 25% from levels posted one year earlier, but similar to volumes from late in 2023. Transactions year to date have been mixed fairly evenly between Class B and Class C complexes, similar to the mix of properties that have changed hands in the past two years. While construction has ramped up in recent years, only about 10% of the properties that have been delivered since 2020 have been sold after being completed.

Looking ahead

The remainder of this year is expected to be particularly active in both new apartment supply and renter demand for units. Development trends have been uneven in recent years, with permitting and starts accelerating before slowing. This year is on pace to mark a peak in annual deliveries, but by the end of the year, the construction pipeline will have thinned to its lowest level since 2021. Multifamily permitting has already begun to slow, a trend that is forecast to continue. The combined results of the surge in deliveries this year will be a modest rise in vacancies and limited rent growth, but the market’s outlook brightens beginning in 2025. Over the longer-term, developers will have a hard time keeping pace with persistent renter demand, which should result in low vacancy rates and steady rent increases going forward.

The investment market will likely regain some momentum in the coming quarters, with the recent rise in cap rates expected to make it easier for deals to get done. Last year, the strongest periods of transaction activity occurred in the second and third quarters, and preliminary indications suggest sales velocity should pick up in the middle part of this year as well. Assuming cap rates remain around 6%, buyers may find it easier for acquisitions to pencil, particularly if interest rates creep lower in the final few months of 2024. Longer term, investors are expected to be drawn to the Inland Empire’s strong population growth outlook. The region is expected to grow at twice the rate of the rest of Southern California over the next 25 years, a period where nearly 1 million new residents will be added.

Learn more

Read the report or contact our Irvine office to learn more.

Read More

Insights

Research to help you make knowledgeable investment decisions